What Is Tax Loss Harvesting? How Does It Work?

Tax loss harvesting is a way of using your existing losses to offset the gains in your portfolio, which can significantly reduce the taxes you owe to the government.

What if there was a way through which you could gain from the decline in your stock portfolio? Sounds intriguing, right?

There’s actually an easy way to do this — tax loss harvesting. In simple terms, tax loss harvesting is a way of using your existing losses to offset the gains in your portfolio, which can significantly reduce the taxes you owe to the government. In this article, we will discuss everything you need to know about tax loss harvesting, including how it works, examples, and things to remember. Continue reading to find out!

What Is Tax Loss Harvesting?

Loss harvesting involves selling securities that have experienced a loss to offset gains realised by selling securities that have appreciated in value. The formula for tax loss harvesting is

Capital Loss - Capital Gain = Taxable Gain or Loss

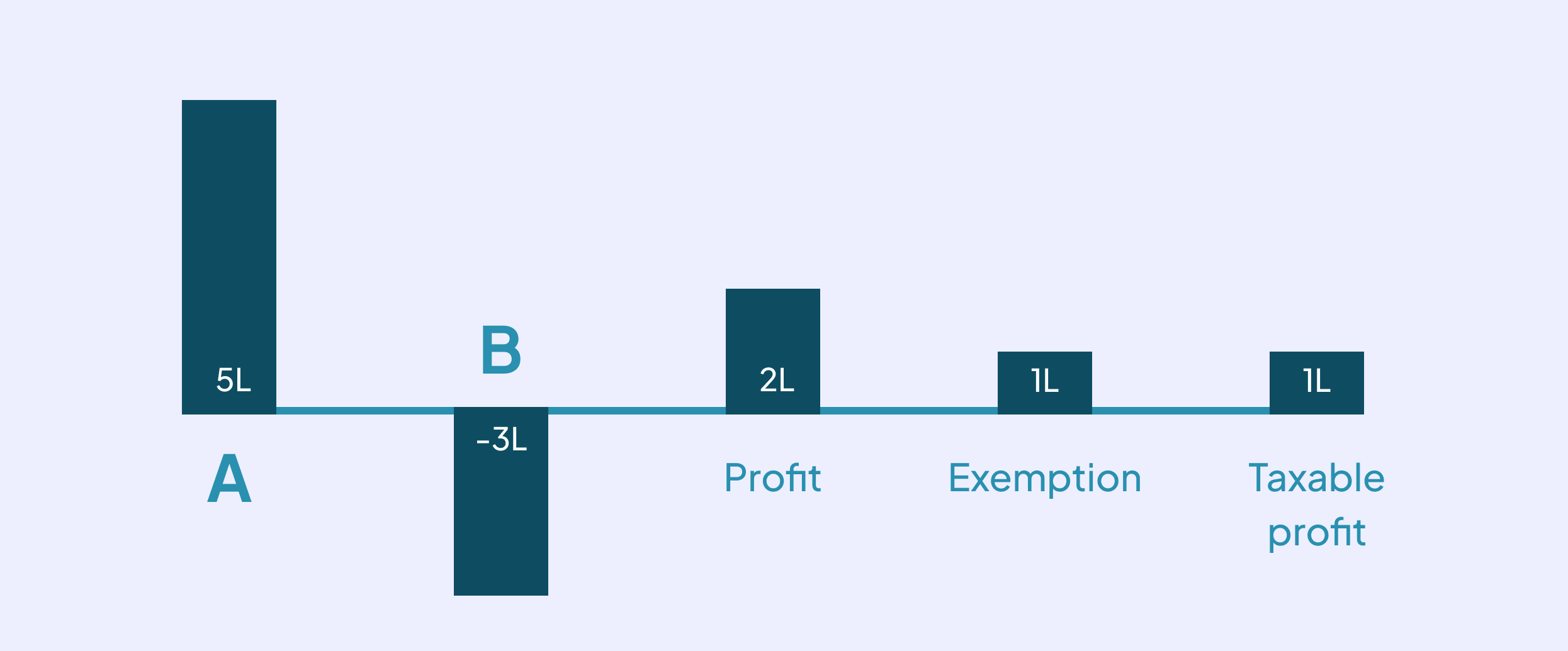

Let’s understand this by going through this example of tax loss harvesting below:

Assume you have two stocks in your portfolio: A and B. Stock A has increased in value, resulting in a long-term capital gain of Rs. 5,00,000. On the other hand, Stock B has decreased in value, resulting in a long-term capital loss of Rs. 3,00,000.

In this case, if you sell Stock A and realise the profit, you will be liable to pay 15% of the 5,00,000, which is Rs 60,000, with the exception of Rs 1,00,000 from long-term capital gains taxes. However, if you sell both stocks, you will have a net long-term capital gain of Rs. 2,00,000 (5,00,000 - 3,00,000). This means you must pay taxes on this capital gain of only Rs 1,00 000 at the applicable tax rate of Rs 15,000.

In this way, you can benefit from the losing stocks in your portfolio to reduce the tax liability on your profit-making stocks. Not only this, you can buy back the losing stocks to hold them for the long term.

How Does Tax Loss Harvesting Work?

Tax loss harvesting involves selling securities in your portfolio that have experienced a capital loss, either short-term or long-term. Short-term capital losses are those that are realised by selling securities held for less than a year, while long-term capital losses are those realised by selling securities held for more than a year.

Also, when you sell securities at a loss that is more than your current profits, any remaining losses can be carried forward for up to eight years and used to offset future capital gains.

Tax harvesting is not a one-time event; it's an ongoing process that involves constantly monitoring your portfolio for opportunities to harvest losses. To maximise its benefits, you should consider implementing this loss harvesting at regular intervals, such as quarterly or annually.

Plus, it helps keep your portfolio's risk and reward balance on point. Along with other tactics, tax loss harvesting is a major key to saving big bucks on taxes. Plus, you can learn different ways to mix up your investments and earn more dough. It won't magically erase all your losses, but it can ease the pain by cutting taxes.

Things To Keep In Mind While Tax Loss Harvesting

Here are some of the following points you should know about tax loss harvesting in India:

- Long-term vs. short-term capital loss: Long-term capital losses can be used to offset long-term capital gains, while short-term capital losses can be used to offset short-term capital gains. It's important to keep even track of your short-term and long-term capital losses separately to maximise your tax savings.

- Offset capital gains: Tax loss harvesting is most effective when you have capital gains to offset. If you have no capital gains in a given year, you can still use up to Rs. 3,00,000 of capital losses to offset your taxable income.

- Invest wisely: While tax harvesting can be a powerful tool to reduce your tax liability, it should not be the sole factor driving your investment decisions. If a stock does not fulfil your investment criteria or investing strategy, you should not hold on to it to harvest the loss.

Where Can You Apply Tax Loss Harvesting?

Below are some of the instruments in India where tax loss harvesting is applicable:

- Equity investments, such as stocks and mutual funds, known for their volatility, are better options for tax harvesting. However, you should be careful about the accurate timing of the sale of securities that have decreased in value. Know the fact that investors can offset capital gains and reduce their tax liability.

- Debt investments, in the form of bonds and Guaranteed Investment Certificates (GICs), mortgages, or preferred shares, can also be used for tax loss harvesting. However, you should know and consider the tax implications of selling debt securities, as they may be subject to different tax rates and rules than equity investments.

Conclusion

Tax loss harvesting in India can be a powerful investment strategy to reduce tax losses and maximise returns. However, you must abide by all the rules and regulations of the Income Tax Act and consider your investment goals before implementing this strategy. By considering these, investors can effectively use tax loss harvesting to minimise their tax burden and achieve their financial objectives.

Summary

- Tax loss harvesting allows investors to use capital losses to offset capital gains in their portfolio, reducing the taxes owed to the government.

- By selling securities that have experienced a loss, investors can offset the gains from profitable securities and potentially lower their tax liability.

- It's important to differentiate between short-term and long-term capital losses and track them separately to maximise tax savings.

- Tax loss harvesting is an ongoing process that involves regularly monitoring the portfolio for opportunities to harvest losses, which can be carried forward for up to eight years.

- While tax loss harvesting can be a valuable strategy, it should not be the sole driver of investment decisions, and investors must consider their overall investment goals and criteria.